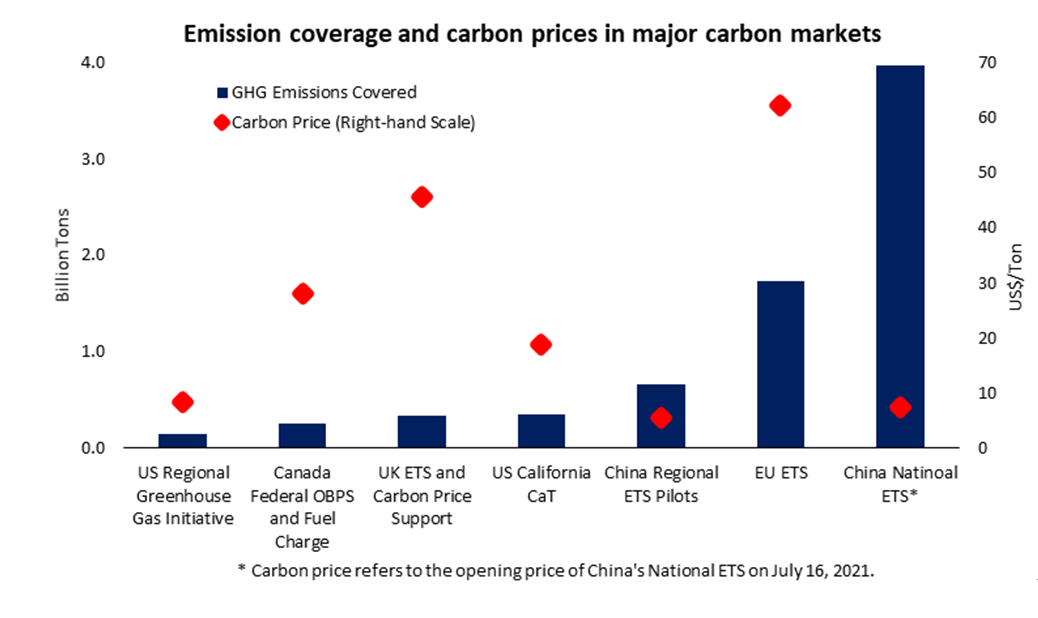

The statistician Nassim Nicholas Talebcoined the term "black swan "to describe improbable, hard-to-predictevents that can have a massive impact on the economy. The authors of a recentreport have now introduced the phrase "green swans" in reference toevents caused by climate change and biodiversity loss. The appearance of green swans is arguablymore predictable than that of black swans, as climate change makes themunavoidable. But there are no historical comparisons to help us understand howclimate and ecological risks such as cyclones, wildfires, droughts and floodsmight affect the banking system, the insurance industry or any number of othereconomic activities. As economic activity is reallocated fromfossil fuels to clean energy sources, some activities will disappear, otherswill emerge and the value of "stranded assets" will plummet. Althoughthis process is necessary, it must be managed in a way that does not createinstability in the financial system. Owing to their financial-stability mandate,central banks, supervisors and macro-prudential authorities have a central roleto play in the green transition. The recent Green Swan Conference organized bythe Bank for International Settlements, the Bank of France, the InternationalMonetary Fund and the Network of Central Banks and Supervisors for Greening theFinancial System pointed to a growing recognition of this fact, though themobilization remains too slow and too timid in some geographic areas. With an eye toward anticipating the effectsof climate risk, the Bank of France was the first central bank to introduce acomprehensive climate stress test for banks and insurance companies. Analyzingthree 30-year climate scenarios-an orderly transition based on a low-carbon strategy; a disorderly,late transition; and a business-as-usual scenario-the test sought toassess banking and insurance portfolios' exposure to both physical andtransition risks. This exercise showed that the Frenchsystem's current exposure is only moderate under the assumptions used. Moreimportant, the climate stress test demonstrated what it will take to improveour understanding of climate risk. There is much more work to do. For example,there is a lack of databases detailing the geographical conditions throughoutglobal value chains. This information is essential to assess physical risks toproduction, and it would also be useful for monitoring social and environmentalgovernance issues more broadly. The increased frequency and severity ofweather-related disasters will gradually come to be reflected in insurancecoverage and costs, affecting profitability and the default rates of loanportfolios in the banking sector. At the same time, bankers and asset managerswill be adjusting their portfolios accordingly. In addition, if the price ofcarbon continues to rise, as it should, they will move away fromcarbon-intensive sec-tors, increasing their exposure to other risk factors. These time-varying behaviors (and their subsidiaryor indirect effects) will matter for financial stability, but they aredifficult to model. Still, a few essential policies would greatly helpmacro-prudential authorities and investors manage the change. First, thoseembarking on the green transition will need a compass: There should be a fullypredictable increase in the carbon price across as wide an economic area aspossible. The European Union could be on the right track with its EmissionsTrading System, wherein the price of carbon has risen from 25 euros ($30) permetric ton in January 2020 to 50 euros per ton today. But progress remainslimited, because the system covers only about 40 percent of EU emissions. Credible commitments to deliver apredictably increasing carbon price are needed to enable investors, regulatorsand monetary policymakers to adjust their strategies in a forward-lookingmanner. In their absence, we will be unable to unleash public and privateinvestment for the structural adjustments needed to reduce the costs of the broadertransition. To achieve this, independent carboncouncils can manage carbon-price inflation in a manner that is similar to howcentral banks manage how inflation affects the prices of goods. Capital requirements for financialinstitutions could be linked to their exposure to a rising carbon price, whichwould change their calculated probability of defaults and losses on theirportfolio. We should expect that private equity firmswill try to acquire risky oil and gas properties, develop them, and sell themat a profit. But we cannot tolerate "below-the-radar" investorsbuying up carbon-intensive assets at fire-sale prices and then operating themin lax jurisdictions. Preventing this will require a high global floor oncarbon prices, carbon border adjustment taxes, or both. A final key climate-policy component ismandatory disclosures of CO2 emissions and a framework for harmonizing those disclosuresglobally in order to enforce universal minimum standards. This idea is alreadygaining momentum and may become more concrete after the 26th UN Climate ChangeConference of the Parties later this year. Transparency is crucial for all market participants.It is incumbent on the institutions in charge of financial stability to ensurethat green swans do not turn black. Vibrancy in China's carbon emissionstrading system will help advance the green transformation of the country'senergy-intensive industries and make green investment a major theme in thecapital market, said experts. Inaugurated on July 16, China's nationalcarbon emissions trading system, which is the world's largest at present, sawtotal trading volume exceed 4.7 million tons in the first five trading days. The carbon emission trading price closed at55.5 yuan ($8.6) per ton on July 22, up 2.06 percent from the previous day. A dual-city mechanism has been adopted forthe national carbon trading system. The Shanghai Environment and EnergyExchange is responsible for building the trading system while the China HubeiEmission Exchange in Wuhan, Hubei province, deals with applications. China's initial carbon trading participantsare the 2,225 electricity companies that are registered with the Hubeiexchange. Chen Li, chief economist at ChuancaiSecurities, said that China's electricity industry will embrace greentransformation, thanks to the carbon emissions trading. As the country will gradually tighten itsgrip on carbon emissions quota, electricity companies that take a slower pacein low-carbon transformation, are sure to purchase quotas from industry peers.In other words, companies taking the lead in low-carbon transformation can expectto reap a windfall, he said. Zhang Xia, chief strategist at ChinaMerchants Securities, said industries known for high carbonemissions-petrochemicals, chemicals, construction materials, steel, nonferrousmetals, paper-making and aviation-will be included in the carbon emissionstrading system during the 14th Five-Year Plan (2021-25) period. Policies will be introduced to guidecompanies in such industries to reduce their carbon emissions. Outdatedproduction capacities will be eliminated from the market more rapidly, he said. Yang Yu, general manager of the researchand innovation department at Hwabao Securities, estimated the amount of carbonemissions included in the carbon emissions trading system will increase to 8billion tons every year with the addition of the eight high-carbon-emissionindustries during the 14th Five-Year Plan period, which will double the currentamount. Ethan Wang, head of investment strategy forwealth management at Standard Chartered China, said climate change-relatedtopics such as carbon neutrality will be one of the major investment themes inChina. The transformation of the country's energy mix will mean clean energiessuch as wind and solar power will replace coal in electricity generationeventually, he said. Yin Zhongshu, chief analyst forenvironmental protection, power equipment and new energy industries atEverbright Securities, said that in the second half of the year, investors canlook for opportunities in companies related to the changes that will revolutionizethe power industry and related segments, including photovoltaic, new energyvehicles, energy storage and wind power. As carbon trading matures, new demand forservices like consultation, verification, management and market-making willemerge. The A-share carbon-neutrality sector hasrisen for three consecutive trading days since Tuesday, according to markettracker Hithink Royalflush Information Network. Trading commenced on China's nationalemissions trading system (ETS) on July 16. With a trading volume of about 4billion tons of carbon dioxide or roughly 12 percent of the total global CO2emissions, the ETS is now the world's largest carbon market. While the traded emission volume is large,the first trading day opened, as expected, with a relatively modest price of 48yuan ($7.4) per ton of CO2. Though this is higher than the global average,which is about $2 per ton, it is much lower than carbon prices in the EuropeanUnion market where the cost per ton of CO2 recently exceeded $50. The ETS has the potential to play animportant role in achieving, and accelerating China's long-term climate goals —of peaking emissions before 2030 and achieving carbon neutrality before 2060.Under the plan, about 2,200 of China's largest coal and gas-fired power plantshave been allocated free emission rights based on their historical emissions,power output and carbon intensity. Facilities that cut emissions quickly willbe able to sell excess allowances for a profit, while those that exceed theirinitial allowance will have to pay to purchase additional emission rights orpay a fine. Putting a price tag on CO2 emissions will promote investment inlow-carbon technologies and equipment, while carbon trading will ensureemissions are first cut where it is least costly, minimizing abatement costs.This sounds plain and simple, but it will take time for the market to developand meaningfully contribute to emission reductions. The initial phase of market development isfocused on building credible emissions disclosure and verification systems —the basic infrastructure of any functioning carbon market — encouragingfacilities to accurately monitor and report their emissions rather thanconstraining them. Consequently, allocations given to power companies have beenrelatively generous, and are tied to power output rather than being set atabsolute levels. Also, the requirements of each individualfacility to obtain additional emission rights are capped at 20 percent abovethe initial allowance and fines for non-compliance are relatively low. Thismeans carbon prices initially are likely to remain relatively low, mitigatingthe immediate financial impact on power producers and giving them time toadjust. For carbon trading to develop into asignificant policy tool, total emissions and individual allowances will need totighten over time. Estimates by Tsinghua University suggest that carbon priceswill need to be raised to $300-$350 per ton by 2060 to achieve carbonneutrality. And our research at the World Bank suggest a broadly applied carbonprice of $50 could help reduce China's CO2 emissions by almost 25 percentcompared with business as usual over the coming decade, while alsosignificantly contributing to reduced air pollution. Communicating a predictable path for annualemission cap reductions will allow power producers to factor future carbonprice increases into their investment decisions today. In addition, experiencefrom the longest-established EU market shows that there are benefits tosmoothing out cyclical fluctuations in demand. For example, carbon emissions naturallydecline during periods of lower economic activity. In order to prevent thisfrom affecting carbon prices, the EU introduced a stability reserve mechanismin 2019 to reduce the surplus of allowances and stabilize prices in the market. Besides, to facilitate the energytransition away from coal, allowances would eventually need to be set at anabsolute, mass-based level, which is applied uniformly to all types of powerplants — as is done in the EU and other carbon markets. The current carbon-intensity basedallocation mechanism encourages improving efficiency in existing coal powerplants and is intended to safeguard reliable energy supply, but it creates fewincentives for power producers to divest away from coal. The effectiveness of the ETS in creatingappropriate price incentives would be further enhanced if combined with deeperstructural reforms in power markets to allow competitive renewable energy togain market share. As the market develops, carbon pricingshould become an economy-wide instrument. The power sector accounts for about30 percent of carbon emissions, but to meet China's climate goals, mitigationactions are needed in all sectors of the economy. Indeed, the authorities planto expand the ETS to petro-chemicals, steel and other heavy industries overtime. In other carbon intensive sectors, such astransport, agriculture and construction, emissions trading will be technicallychallenging because monitoring and verification of emissions is difficult.Faced with similar challenges, several EU member states have introducedcomplementary carbon taxes applied to sectors not covered by an ETS. Suchcarbon excise taxes are a relatively simple and efficient instrument, chargedin proportion to the carbon content of fuel and a set carbon price. Finally, while free allowances are stillgiven to some sectors in the EU and other more mature national carbon markets,the majority of initial annual emission rights are auctioned off. This not onlyensures consistent market-based price signals, but generates public revenuethat can be recycled back into the economy to subsidize abatement costs, offsetnegative social impacts or rebalance the tax mix by cutting taxes on labor, generalconsumption or profits. So far, China's carbon reduction effortshave relied largely on regulations and administrative targets. The launch ofthe national ETS has laid the foundation for a more market-based policyapproach. If deployed effectively, China's carbon market will create powerfulincentives to stimulate investment and innovation, accelerate the retirement ofless-efficient coal-fired plants, drive down the cost of emission reduction,while generating resources to finance the transition to a low-carbon economy. |